Best Perth Suburbs for a First-Time Cafe Owner (2026)

Locatalyze Research Team

Location intelligence, Locatalyze

The best suburbs to open a cafe in Perth are not the same list for a first-time owner as they are for someone on their third site. The ranking changes when the operator changes, and most cafe-location advice ignores that. A scored suburb is a base rate for an average operator running an average offer. A first-timer is not average. They are slower at the pass, looser on cost control, still learning their own catchment, and carrying less capital to absorb a bad first year. The criteria that suit them are different from the criteria that suit an experienced operator, and the difference is the whole point of this ranking.

Here is the uncomfortable version. Mount Lawley, Subiaco and Leederville are genuinely the strongest cafe suburbs in Perth on the Locatalyze model, scoring 79, 78 and 77 respectively, all flagged GO (Locatalyze suburb model, 2026). They are also the most expensive places in the metro to put a cafe, with inner-premium rents running roughly $3,500 to $6,500 a month for a small tenancy (Locatalyze suburb model, 2026). Those two facts are not a coincidence. The high score and the high rent describe the same thing: a suburb where demand is real, the market knows it, and the lease has already priced it in. An experienced operator survives that, because they can execute well enough to earn the margin the rent demands. A first-timer who signs in Mount Lawley is paying experienced-operator rent without experienced-operator margins. They have bought the prestige and inherited the cost base, and they are trying to clear it while still making beginner mistakes.

The first-time-owner filter re-weights the model. It pulls hard toward rent affordability, away from peak-competition prestige, and toward growing rather than peaked suburbs and demographics that forgive a less-polished offer. Run that filter over Perth and the recommendation is not the top of the GO list. It is the mid-ring: Victoria Park at a cafe score of 74 and Morley at 72, both at materially lower rent of roughly $2,500 to $5,000 a month, both with the kind of catchment that does not punish you for charging a fair price rather than a precious one (Locatalyze suburb model, 2026). That is the risk-adjusted first cafe. It is not the most exciting site on the board, and that is exactly why it is the right one.

The base rates make the stakes plain. Across the Australian economy, only 54% of cafe, restaurant and takeaway businesses trading in June 2020 were still trading four years later, against 64% for all businesses (Tourism Research Australia, *Tourism Businesses in Australia: June 2019 to 2024*, built on ABS data). Accommodation and Food Services was the second-largest source of corporate insolvency in Australia in FY2023–24, at 15% of all external administrations (ASIC, *Annual insolvency data*, FY2023–24). A first-timer does not get to pretend those numbers are about other people. The site decision is the single biggest lever they hold before opening, and choosing experienced-operator territory on a beginner's skill set is how a survivable mistake becomes a terminal one.

How the ranking is built: the five-factor model and the first-timer filter

Most cafe-location lists rank suburbs on atmosphere, a leasing agent's optimism, or a single foot-traffic number stripped of context. This one does not. Each Perth suburb is scored on five factors — demand, rent pressure, competition, seasonality and tourism — every one on a one-to-ten scale, and the cafe score is a weighted blend tuned for the cafe format specifically.

Demand is the catchment's capacity to spend on cafe trade: residential density and income, daytime worker population, and the depth of the daily routine that brings people past a counter more than once a week. Rent pressure is the cost-side mirror, measuring how hard the local lease market squeezes effective rent against the revenue the catchment can realistically produce. Competition measures saturation — cafe density weighed against the catchment that has to feed it, not a raw count of shopfronts. Seasonality penalises suburbs whose trade swings hard across the year, because a single-peak calendar cannot amortise twelve months of fixed rent. Tourism is a demand booster where it is genuine, but it is the weakest and most fragile of the five drivers, because tourist trade is volatile and concentrated into dayparts the operator does not control. The output is a cafe score out of 100 and a verdict — GO, CAUTION or what the engine flags as RISKY — so a high score in a structurally fragile suburb cannot quietly pass as a recommendation.

The first-timer filter is a re-weighting of that base model, and it moves in one consistent direction. It raises the weight on rent affordability, because a beginner's margin is thinner and their cost control is looser, so a low rent floor is worth more to them than to an operator who can hold food cost to target in their sleep. It lowers the weight on peak-competition prestige, because a saturated, sophisticated strip is a field where an undifferentiated first offer gets ignored, and a first offer is almost always undifferentiated. It favours growing over peaked suburbs, because a suburb still adding catchment gives a new operator room to grow into rather than a fully-priced market to fight over. And it favours forgiving demographics — a catchment that rewards a fair, honest offer over one that demands a polished, premium execution the operator cannot yet deliver.

None of this changes the underlying scores. Mount Lawley is still a 79. What changes is who the score is good advice for. The five-factor model answers "where is the strongest cafe demand-to-cost ratio in Perth". The first-timer filter answers a narrower and more useful question for a beginner: "where can I afford to make my first-year mistakes and still be trading at the end of it".

The best suburbs to open a cafe in Perth, by tier

The Perth suburbs that matter for this decision fall into four groups. Each tier has a distinct rent profile and a distinct risk character, and the first-timer's path runs straight through the second one.

Inner premium — experienced-operator territory

Mount Lawley (cafe 79, GO), Subiaco (78, GO) and Leederville (77, GO) are the top of the board (Locatalyze suburb model, 2026). They earn it: deep demand, established cafe cultures, affluent and reliable catchments. The 2021 Census puts Mount Lawley's median weekly household income at $2,108 and Subiaco's at $2,219, both well above the metro norm (ABS, *2021 Census, Mount Lawley (SAL)*; ABS, *2021 Census, Subiaco (SAL)*). That income is real and it spends on coffee. The catch is the rent. Inner-premium tenancies run roughly $3,500 to $6,500 a month for a small site (Locatalyze suburb model, 2026), and the catchment that justifies it is also a catchment that has tasted a lot of very good cafes and will notice when yours is merely fine.

This is where an experienced operator should look, and where a first-timer should not. The score is high because the suburb rewards execution, and execution is exactly the thing a beginner has not built yet. Sign in Subiaco on a first cafe and the rent is set by what a polished operator can earn from that affluent catchment, while the revenue is set by what a learning operator actually earns. The gap between those two numbers is the failure.

Mid-ring — the first-timer sweet spot

Victoria Park (cafe 74, GO) and Morley (72, CAUTION) are the recommendation (Locatalyze suburb model, 2026). Both carry strong viability at a rent floor a full tier below the inner-premium suburbs — roughly $2,500 to $5,000 a month (Locatalyze suburb model, 2026) — and both have catchments that forgive a less-polished offer rather than punishing it.

Victoria Park is the cleaner of the two. A cafe score of 74 and a GO verdict put it just below the inner-premium leaders on viability, but its rent floor sits in the mid-ring, not the premium tier. The 2021 Census records a median weekly household income of $1,828 across a population of 9,334 (ABS, *2021 Census, Victoria Park (SAL)*) — comfortably above subsistence, comfortably below the Subiaco-Mount Lawley premium, and exactly the profile that spends steadily on cafe trade without demanding a $7 single-origin pour-over to feel served. The Albany Highway strip has an established, unpretentious food culture that a competent new cafe can join rather than having to out-execute. For a first-time owner, that combination — GO-grade viability, mid-ring rent, a catchment that rewards honest value — is the strongest risk-adjusted entry on the Perth board.

Morley carries a CAUTION rather than a GO, and the reason is instructive rather than disqualifying. Its cafe score of 72 reflects solid demand across a large catchment: the 2021 Census records 22,539 residents at a median weekly household income of $1,583 (ABS, *2021 Census, Morley (SAL)*). That is a big, working catchment at a moderate income — lower than Victoria Park, which is why the CAUTION — but it is a catchment that turns up, spends consistently, and does not expect inner-city positioning. The mid-ring rent floor applies here too. For a first-timer who reads the CAUTION correctly — Morley wants a value-led, high-throughput offer, not a precious one — it is a genuinely workable first site at a forgiving cost base. Read it wrong, and over-build a premium fitout for a $1,583-median catchment, and the CAUTION becomes the reason it fails.

High volume and CBD — volatile, not beginner-friendly

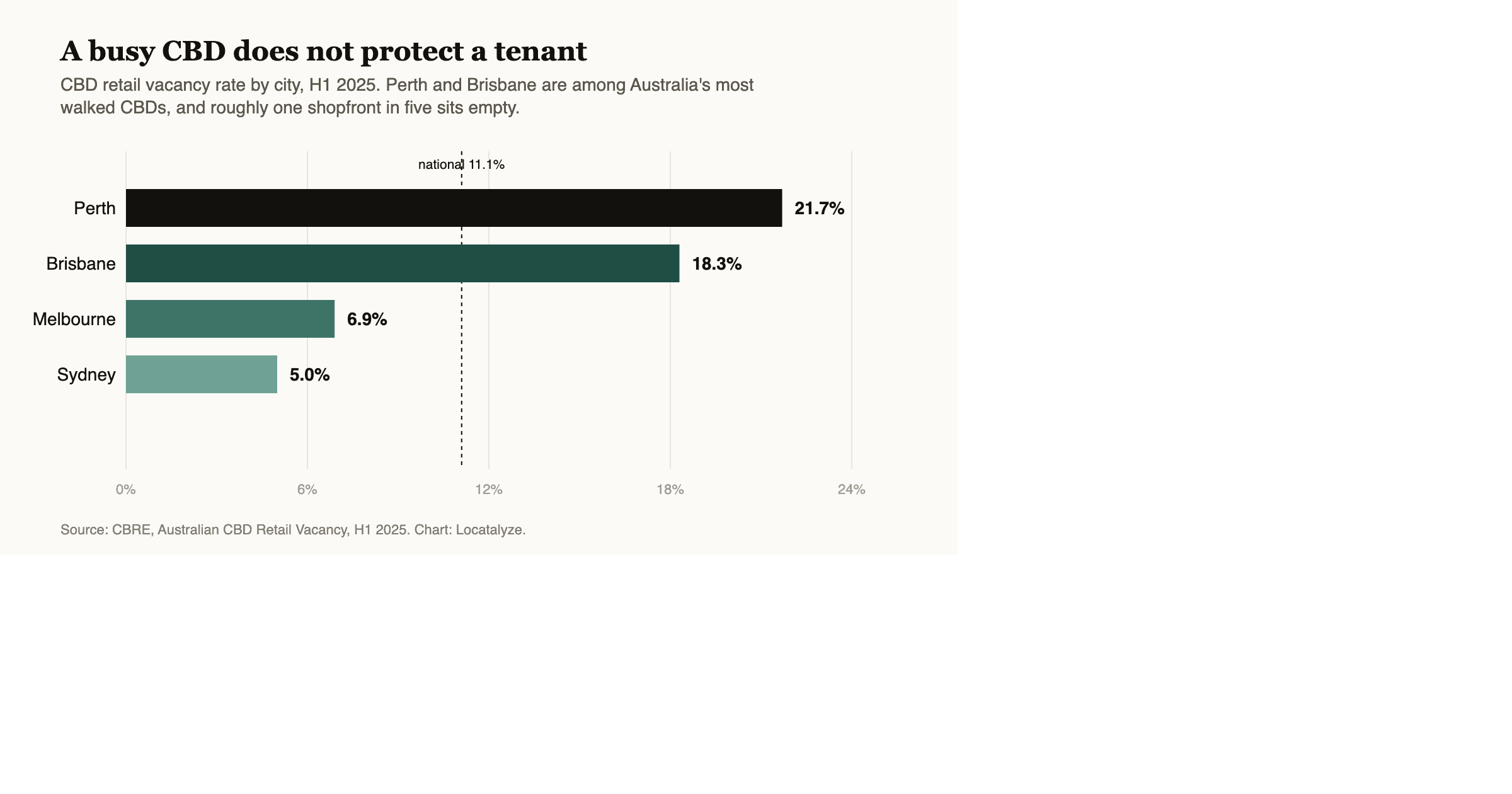

Northbridge (cafe 67, CAUTION), Perth CBD (63, CAUTION) and Fremantle (65, CAUTION) trade high volume against high occupancy cost (Locatalyze suburb model, 2026). The rent range alone tells the story — anywhere from $4,000 to $15,000 a month depending on the site (Locatalyze suburb model, 2026). These are demand-rich but volatile: heavily weighted to dayparts and seasons the operator does not control, exposed to office-occupancy swings and tourist cycles, and saturated with established competition. An experienced operator can run a high-volume site because they can flex labour against the peaks and survive the troughs. A first-timer signing a $9,000-a-month CBD tenancy is underwriting a cost base that assumes peak trade they have no track record of producing. The volume looks like opportunity. The occupancy cost is the trap.

The CBD context is worse than the suburb score alone suggests. Perth's CBD retail vacancy hit 21.7% in the first half of 2025 — the highest of any Australian CBD, against a national average of 11.1% (CBRE, *Australian CBD vacancy*, H1 2025). High vacancy is not a discount opportunity for a beginner. It is a signal that the foot-traffic and trade assumptions a CBD lease is priced on have softened, and a first-timer is the least equipped operator to carry a site through that.

Outer traps — market signals, not discounts

Joondalup (cafe 63, RISKY), Midland (63, RISKY) and Armadale (65, RISKY) look cheap, and the cheapness is the warning, not the offer (Locatalyze suburb model, 2026). Joondalup is oversaturated — the chains hold the viable positions and a new independent is fighting for the leftovers. Midland carries commercial vacancy above 18%, which is the kind of structural softness that does not reward a new entrant. Armadale's household income runs about 26% below the Perth median, which constrains specialty pricing — the catchment cannot support the average ticket a specialty cafe needs to clear its costs (Locatalyze suburb model, 2026). These are market signals telling a careful operator to stay out. A first-timer reading low rent as a bargain in these suburbs is misreading a structural problem as a discount.

This is the suburb-level view. The live, full-coverage version of this ranking scores all 69 Perth suburbs in the live, full-coverage Perth version of the Locatalyze model, with every CAUTION and RISKY suburb included so the line between the tiers is visible rather than implied.

The recommendation, stated plainly

For a first-time owner, Victoria Park and Morley beat the prestige inner-premium GO suburbs, and they beat them on the metric that decides whether a first cafe survives its first year: the gap between the rent the lease assumes and the revenue a learning operator can actually produce.

Mount Lawley, Subiaco and Leederville carry higher scores. They also carry a rent floor that only a confident execution can clear, and a catchment refined enough to notice when the execution is not there yet. Victoria Park and Morley carry slightly lower scores, a rent floor a full tier cheaper, and catchments that reward a fair, well-run, unpretentious offer — which is the only kind of offer a first-timer can reliably deliver in year one. The lower score is the better advice, because the score is a base rate for an average operator and the first-timer is not buying the average suburb. They are buying the room to be below average for a while and still be trading when they climb out of it.

First-timer versus experienced operator: the same suburbs, different picks

The clearest way to see the filter at work is to set the two operator types side by side on the same Perth suburbs. The viability scores are identical — the suburb does not change — but the right pick diverges, because the constraint that binds each operator is different.

The reasoning splits cleanly along one axis: what binds each operator. A first-timer is bound by execution risk and the rent floor. Their margin is thinner, their cost control is looser, and a high fixed rent removes the slack they need to survive the learning curve. So they should pick the suburb where viability is still strong but the rent is forgiving — Victoria Park first, Morley second — and treat the lower rent floor as insurance against their own inexperience. An experienced operator is bound by the demand ceiling and margin upside. They can hold food and labour cost to target, so they can clear a premium rent, and what they want is the deepest, most affluent catchment they can find to maximise the margin their execution can extract. So they should pick Mount Lawley, Leederville or Subiaco, where the higher rent is a price worth paying for a catchment that rewards a polished offer.

All values: Locatalyze suburb model, 2026; income context from ABS 2021 Census.

The matrix is not saying the inner-premium suburbs are bad. It is saying they are bad *first* cafes. The same Mount Lawley that breaks a beginner is a strong site for an operator on their third cafe who already knows how to run the pass, hold cost, and earn the rent. The suburb did not change between those two operators. The skill carrying the rent did.

Where the rent tiers sit against the score

The reason the first-timer filter lands on the mid-ring becomes obvious once the rent tiers are plotted against the cafe score. The inner-premium suburbs sit top-right: high score, high rent. The mid-ring sits in the middle band — still high on score, materially lower on rent. That middle band is the forgiving zone, and it is where a first cafe belongs.

The pattern is structural, not coincidental. Rent is fixed by the lease and revenue is capped by the catchment and by the operator's ability to convert it. An inner-premium suburb at the top-right pairs a strong score with a rent that assumes a strong operator; the arithmetic only works if the execution is there. A mid-ring suburb in the forgiving band pairs a near-equal score with a rent that leaves slack in the rent-to-revenue ratio — slack a first-timer needs and an experienced operator does not. The outer RISKY suburbs sit low-left for a different reason: their cheap rent reflects a structural problem in the catchment, not a bargain. The forgiving zone is the only place on the chart where low rent and strong viability appear together, and that pairing is precisely what a first cafe should buy.

What this ranking does not tell you

The honest limitations matter as much as the ranking, and for a first-timer they matter more, because a beginner is the operator most likely to over-read a suburb score as a guarantee.

It is a suburb-level model, not a shopfront model. A suburb score is a base rate for the area; the specific corner can sit well above or well below it. A Victoria Park cafe on a quiet block can underperform the suburb's 74, and a Subiaco cafe on a prime corner can beat the suburb's 78. The score narrows the search. It does not pick the lease.

It does not benchmark the actual rent. The model reads rent *pressure* — the local market's tendency to price hard against achievable revenue — not the dollar figure on the lease under negotiation. The tier ranges quoted here are the engine's published bands (Locatalyze suburb model, 2026), and two tenancies in the same suburb can carry very different effective rents depending on frontage, incentive and term. The factor tells you the climate; it cannot read the contract.

It does not capture operator quality, capital structure or timing. The first-timer filter is a re-weighting toward suburbs that forgive inexperience; it is not a substitute for the experience itself. A forgiving suburb run badly still fails, and the model isolates none of management skill, food quality or the capitalisation runway that decides whether a new cafe reaches the far side of its first year (Tourism Research Australia, June 2019 to 2024). Suburb dynamics also move — a competition reading that is manageable today can tighten as a strip matures.

And it does not predict individual outcomes. The base rate in Australian hospitality is roughly 46% closure over four years, and the second-highest corporate insolvency share of any sector (Tourism Research Australia, June 2019 to 2024; ASIC, FY2023–24). Choosing a forgiving mid-ring suburb moves a first-timer toward the better tail of that distribution. It does not exempt them from it. The full mechanics of those base rates sit in the Australian cafe failure rate analysis, and the rent side of the decision — how effective rent actually moves across markets and formats — is in the companion read on commercial rent per square metre across Australia.

What this means before you sign a lease

The practical implication for a first-time owner is a sequence, not a single answer. Start with the operator-aware shortlist: in Perth in 2026 that is Victoria Park first and Morley second, with the inner-premium GO suburbs — Mount Lawley, Subiaco, Leederville — deliberately set aside as second-cafe territory, and the CBD, high-volume and outer-RISKY suburbs set aside as traps that look like opportunities. Then prove the specific site, because a suburb average cannot price the corner.

Two tenancies a few doors apart on the same Albany Highway stretch in Victoria Park can be different businesses — different walk-past, different effective rent, different competition inside the 500-metre catchment. That gap between a suburb score and a site decision is the gap a single-address analysis closes. The same five-factor model extends across formats and cities through the broader location analysis platform, and an operator weighing Perth against the east coast can run the same logic over the best suburbs to open a cafe in Melbourne, where the market is more saturated and the trade-offs sharper.

Before committing, see the footfall, competition and rent-fit picture for the specific shopfront rather than the suburb mean — for an operator who has not done this before, that is the difference between a hunch and a decision.

Free location score, map, data confidence and PROCEED / VERIFY / AVOID recommendation. Modelled financials stay optional.

Analyse your addressThe first-timers who are still trading in four years are rarely the ones who signed the most prestigious lease they could reach. They are the ones who picked the suburb that forgave their inexperience, proved the specific site carried its rent, and grew into the better postcodes once they had the execution to earn them. Start with the forgiving suburb. Finish with the address. Save the prestige for the second cafe.

References

CBRE, *Australia's CBD vacancy rate tightens — H1 2025*: Perth CBD retail vacancy of 21.7% in the first half of 2025, the highest of any Australian CBD, against a national average of 11.1%. cbre.com.au

Australian Securities and Investments Commission, *Annual insolvency data, FY2023–24*: Accommodation and Food Services the second-largest source of corporate insolvency, 15% of all external administrations. asic.gov.au

Tourism Research Australia, *Tourism Businesses in Australia: June 2019 to 2024* (built on ABS Counts of Australian Businesses): 54% of cafes, restaurants and takeaway businesses operating in June 2020 were still operating in June 2024, against 64% for all Australian businesses. tra.gov.au

Australian Bureau of Statistics, *2021 Census of Population and Housing, General Community Profile (Suburbs and Localities)*: Victoria Park population 9,334, median weekly household income $1,828; Subiaco population 9,940, median weekly household income $2,219; Mount Lawley population 11,328, median weekly household income $2,108; Morley population 22,539, median weekly household income $1,583. abs.gov.au

Locatalyze suburb model, 2026: cafe scores, verdicts, rent tiers and the five-factor demand, rent pressure, competition, seasonality and tourism readings for 69 Perth suburbs. Mount Lawley 79 (GO), Subiaco 78 (GO), Leederville 77 (GO), Victoria Park 74 (GO), Morley 72 (CAUTION); inner-premium rents ~$3,500–6,500/mo, mid-ring ~$2,500–5,000/mo, high-volume/CBD ~$4,000–15,000/mo. Market signals: Joondalup oversaturated, Midland commercial vacancy above 18%, Armadale household income about 26% below the Perth median.

First-time operator checks for Perth

Related reading

Frequently asked questions

About the author

Locatalyze Research Team

Location intelligence, Locatalyze

The Locatalyze research team builds the location-scoring models behind the platform and writes up what the data shows for Australian operators.

Tools first — then a full report for your address

Free rent, viability, and break-even checks. Upgrade when you are ready for competitors, map, and numbers for a specific site.

No signup required for tools