Best Suburbs to Open a Cafe in Melbourne in 2026 (Ranked by Demand, Rent & Competition)

Locatalyze Research Team

Location intelligence, Locatalyze

The best suburbs to open a cafe in Melbourne in 2026 are not the ones with the most people walking past the door. In the most saturated hospitality market in the country, the winning sites are the ones with the strongest ratio of demand to rent pressure to competition for the format you can actually run. Brunswick Street in Fitzroy at 8am looks like easy money. It is not. Every metre of that footpath is already priced, already contested, and already serving people who have four other coffees within ninety seconds of where they are standing. Foot traffic is the input every first-time operator over-weights, and it is the one the market has already capitalised into the rent.

The thesis of this ranking is narrow and it is uncomfortable. Across 60 Melbourne suburbs scored by the Locatalyze suburb model, the single strongest driver of the cafe score is not demand. It is rent pressure, and it pulls the other way — the correlation between cafe score and rent pressure is −0.58, stronger than demand's +0.49 and far stronger than tourism's +0.18 (Locatalyze suburb model, 2026). Read plainly: the suburbs that score best for a cafe are disproportionately the ones where demand is real but the rent has not yet caught up to it. That is the whole game. A suburb where demand is a 9 and rent pressure is a 4 will out-rank a suburb where demand is a 10 and rent pressure is a 7, because the second site forces you to carry a cost base your trade cannot reliably cover.

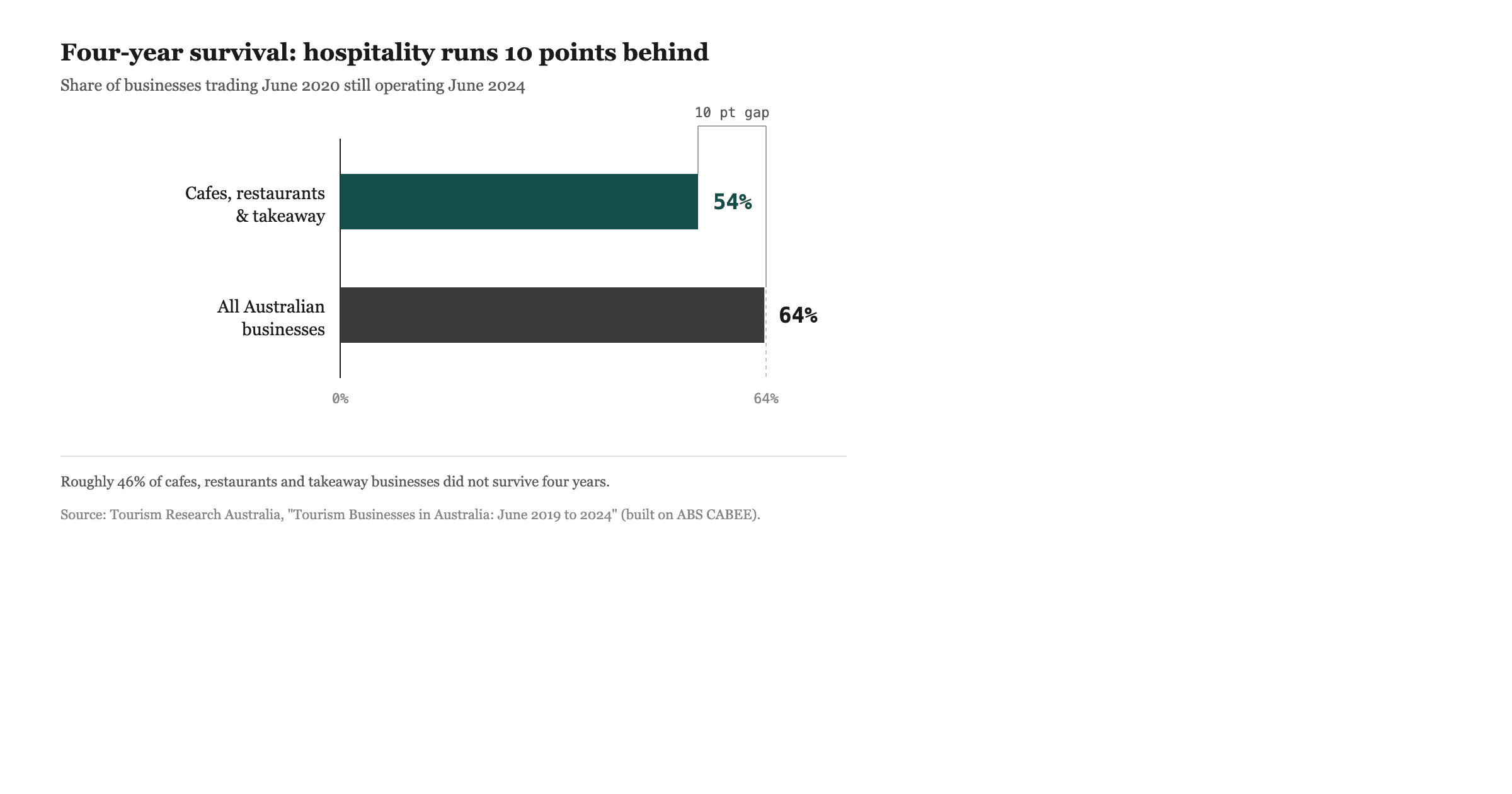

This matters because the base rates in Australian hospitality are punishing. Of every 100 cafes, restaurants and takeaway businesses trading in June 2020, only 54 were still trading four years later, against 64 across the whole economy (Tourism Research Australia, *Tourism Businesses in Australia: June 2019 to 2024*, built on ABS data). Accommodation and Food Services was the second-largest source of corporate insolvency in Australia in FY2023–24, accounting for 15% of all external administrations despite being a fraction of the business base (ASIC, *Annual insolvency data*, FY2023–24). Choosing the wrong Melbourne suburb does not give you a slow, recoverable problem. It gives you the eighteen-month version of that statistic.

So this is a ranking built to respect the saturation, not to pretend it away. There is no easy money on Brunswick Street. There is, however, a defensible edge in the suburbs where the demand-to-rent ratio still works, and the rest of this piece is about finding them and naming the format and the primary risk for each.

How the ranking is built: the five-factor model

Most cafe-location listicles rank suburbs on vibe, a property agent's optimism, or a single foot-traffic number lifted out of context. This one does not. Each suburb is scored on five factors, every one on a one-to-ten scale, and the cafe score is a weighted blend of them tuned for the cafe format specifically.

The five factors are demand, rent pressure, competition, seasonality and tourism.

Demand is the catchment's capacity to spend on cafe trade — residential density and income, daytime worker population, and the depth of the daily routine that brings people past a counter more than once a week. Rent pressure is the cost-side mirror: how hard the local lease market squeezes gross effective rent against the revenue the catchment can realistically produce. Competition measures saturation — not a raw count of cafes, but density weighed against the catchment that has to feed them. Seasonality penalises suburbs whose trade swings hard across the year, because a single-peak calendar cannot amortise twelve months of fixed rent. Tourism is a demand booster where it is real, but it is the weakest of the five drivers and the most fragile, because tourist trade is volatile and concentrated into dayparts you do not control.

The blend is deliberately not symmetric. Because the engine's own correlations show rent pressure is the strongest negative driver of the cafe score and demand the strongest positive one (Locatalyze suburb model, 2026), the model treats a low rent-pressure reading as close to as valuable as a high demand reading. Competition discounts the score where saturation outpaces catchment. Seasonality and tourism are adjustments at the margin, not headline drivers. The result is a cafe score out of 100 and a broader composite score that folds in formats beyond cafes; for this ranking the cafe score leads and the composite sits alongside it as a cross-check. Each suburb also carries a verdict — GO, CAUTION or what the engine flags as RISKY — so a high score in a structurally fragile suburb cannot quietly pass as a recommendation.

Two things this model is not. It is not a foot-traffic ranking; raw pedestrian volume is an input to demand, not the output. And it is not a guess about your specific shopfront. A suburb score is a base rate for the area. The corner you actually lease can sit well above or well below it, which is why the closing section points you at running your own address rather than trusting the suburb average.

The best suburbs to open a cafe in Melbourne, ranked

What follows is the cafe score, composite, verdict and the three load-bearing factors — demand, rent pressure and competition — for each suburb, with a recommended format and the primary risk. All factor values are from the Locatalyze suburb model, 2026.

1. Fitzroy — cafe 87, composite 85, GO

Demand 10, rent pressure 4, competition 3. Fitzroy is the rare Melbourne suburb that scores a perfect demand reading without the rent pressure that usually rides alongside it, and its competition factor of 3 is unusually low for an inner suburb (Locatalyze suburb model, 2026). That combination is why it sits clear at the top. The catchment is deep, the routine is daily, and the saturation reading suggests there is still room inside it. Format: a specialty all-day cafe with a strong brunch daypart and a defensible coffee program — Fitzroy customers will pay for quality and notice when it slips. Primary risk: the suburb's reputation prices the prime Brunswick and Gertrude Street frontages aggressively, so the suburb-level rent-pressure reading of 4 will not hold on the marquee corners. Lease one street back and the ratio that earns the 87 stays intact; pay for the trophy frontage and you have bought a worse business.

2. Brunswick — cafe 79, composite 74, GO

Demand 9, rent pressure 4, competition 5. Brunswick is the clearest of the high-ratio plays: near-top demand at low rent pressure, with competition only moderate (Locatalyze suburb model, 2026). It is the suburb the model rewards for exactly the reason the thesis describes — strong trade that the lease market has not fully capitalised. Format: a neighbourhood cafe with a roastery or wholesale-coffee angle, leaning into Brunswick's maker culture. Primary risk: Sydney Road competition is real and the competition factor of 5 understates how clustered the best stretches are; pick a block with genuine residential catchment behind it rather than a thin retail strip.

3. Preston — cafe 78, composite 73, GO

Demand 8, rent pressure 3, competition 4. Preston is the model's quiet favourite. A rent-pressure reading of 3 against a demand reading of 8 is one of the strongest demand-to-rent ratios in the entire Melbourne set (Locatalyze suburb model, 2026). Format: a value-conscious all-day cafe serving a gentrifying but still price-sensitive catchment — High Street and the area around Preston Market reward honest pricing over precious positioning. Primary risk: the catchment is still in transition, so demand is real but not yet uniformly affluent; over-build the fitout and you price out the regulars who actually carry weekday trade.

4. Footscray — cafe 78, composite 73, GO

Demand 8, rent pressure 3, competition 4. Footscray mirrors Preston almost exactly on the numbers and for the same reason — strong demand, the lowest tier of rent pressure, manageable competition (Locatalyze suburb model, 2026). Format: a cafe that works with, not against, the suburb's established food culture; a coffee-led offer with a tight, well-executed menu rather than a generic brunch template. Primary risk: the catchment's spending profile is uneven block to block, and parts of the centre carry vacancy and transition risk. The suburb score is strong; the specific street matters more here than almost anywhere else on this list.

5. Richmond — cafe 78, composite 75, GO

Demand 9, rent pressure 5, competition 4. Richmond carries the highest composite of the top five (75) on the back of a 9 demand reading, but its rent pressure of 5 is a full two points above Preston and Footscray (Locatalyze suburb model, 2026). The trade is there; you simply pay more of it back in rent. Format: a high-throughput cafe near the Swan Street or Bridge Road retail and worker catchment, built for volume across multiple dayparts. Primary risk: the rent pressure is the constraint. Richmond punishes a single-daypart model, because the rent assumes you trade hard across the day.

6. Camberwell — cafe 77, composite 72, GO

Demand 8, rent pressure 4, competition 4. Camberwell is the established-affluent option that still keeps a workable ratio: solid demand, moderate rent pressure, moderate competition (Locatalyze suburb model, 2026). Format: a polished, family-oriented cafe serving an affluent residential catchment with strong weekend trade. Primary risk: weekend-weighted demand. An affluent residential suburb can trade beautifully on Saturday and thinly on a wet Tuesday, so the weekday base has to be stress-tested before signing.

7. Pakenham — cafe 76, composite 70, GO

Demand 7, rent pressure 3, competition 3. Pakenham is the growth-corridor entry, and it earns its place through the lowest competition and rent pressure on the GO list (Locatalyze suburb model, 2026). Demand is a notch lower at 7, but the saturation is genuinely thin. Format: a destination family cafe with parking and space — outer-corridor trade is car-led, not walk-past-led, and the format has to suit that. Primary risk: demand depth. Growth corridors promise tomorrow's catchment; you have to trade on today's, and the gap between projected and current population is where corridor cafes most often run short of runway.

8. Carlton — cafe 75, composite 73, GO

Demand 9, rent pressure 5, competition 5. Carlton has the demand of an inner-city heavyweight but pays for it on both rent pressure and competition, each at 5 (Locatalyze suburb model, 2026). The student and university catchment is large but price-sensitive and seasonal. Format: a high-volume, efficiently-run cafe geared to the Lygon Street and university foot traffic, with a coffee-led offer that turns tables fast. Primary risk: the competition and the academic calendar together. Saturation is high and a chunk of the catchment empties out between semesters.

9. Northcote — cafe 75, composite 71, GO

Demand 8, rent pressure 4, competition 5. Northcote sits in the sweet spot of the inner-north corridor — strong demand, low rent pressure, but competition has climbed to a 5 as the suburb has matured (Locatalyze suburb model, 2026). Format: a distinctive neighbourhood cafe with a clear point of difference; the High Street catchment is discerning and already well-served. Primary risk: competition. The rent ratio still works, but you are entering a crowded, sophisticated field where an undifferentiated offer gets ignored.

10. Box Hill — cafe 75, composite 70, GO

Demand 8, rent pressure 3, competition 6. Box Hill is the most interesting outlier in the top tier. It carries strong demand and the lowest tier of rent pressure, which is why it scores 75, but its competition reading of 6 is the highest on the GO list (Locatalyze suburb model, 2026). Format: a cafe that suits the suburb's deep Asian dining and grocery culture rather than competing head-on with it — a complementary coffee-and-light-food offer near the transport and retail hub. Primary risk: saturation. The demand-to-rent ratio is excellent; the competition factor is the thing that can starve a generic entrant.

11. Hawthorn — cafe 74, composite 69, GO

Demand 8, rent pressure 5, competition 4 (Locatalyze suburb model, 2026). Hawthorn is solid-affluent with a university overlay, demand steady and competition contained, but rent pressure at 5 trims the ratio. Format: a refined cafe serving residents and Swinburne foot traffic, weekday-capable rather than weekend-only. Primary risk: rent pressure against a partly seasonal student catchment.

12. St Kilda — cafe 71, composite 72, GO

Demand 9, rent pressure 6, competition 5, with a tourism reading of 8 — the highest on this list (Locatalyze suburb model, 2026). St Kilda is the cautionary case at the bottom of the GO band, and it is instructive. Its composite (72) actually exceeds its cafe score (71), because the broader model rewards the tourism and demand more than the cafe-specific lens does. For a cafe, the rent pressure of 6 and the heavy reliance on tourism are penalties. Format: a cafe built to ride tourist seasonality without depending on it — a strong local weekday base with summer upside, not the reverse. Primary risk: seasonality and tourism volatility. A St Kilda cafe that lives on summer foot traffic dies over a wet winter; the tourism that lifts the composite is the same factor that makes the cafe fragile.

Two more sit just inside the GO band and round out a fourteen-suburb field: South Yarra (cafe 75, composite 74; demand 10, rent pressure 7, competition 5) trades top-tier demand for high rent pressure, the classic pay-to-play inner suburb; and Collingwood (cafe 74, composite 72; demand 9, rent pressure 5, competition 6) offers Fitzroy-adjacent demand with a higher competition reading.

This is the suburb-level view. The live, full-coverage version of this ranking scores all 60 Melbourne suburbs in the Locatalyze Melbourne model, with the CAUTION and RISKY tiers — the suburbs this article deliberately keeps off the recommendation list — included so you can see where the line falls.

The analytical point: ratio beats prestige

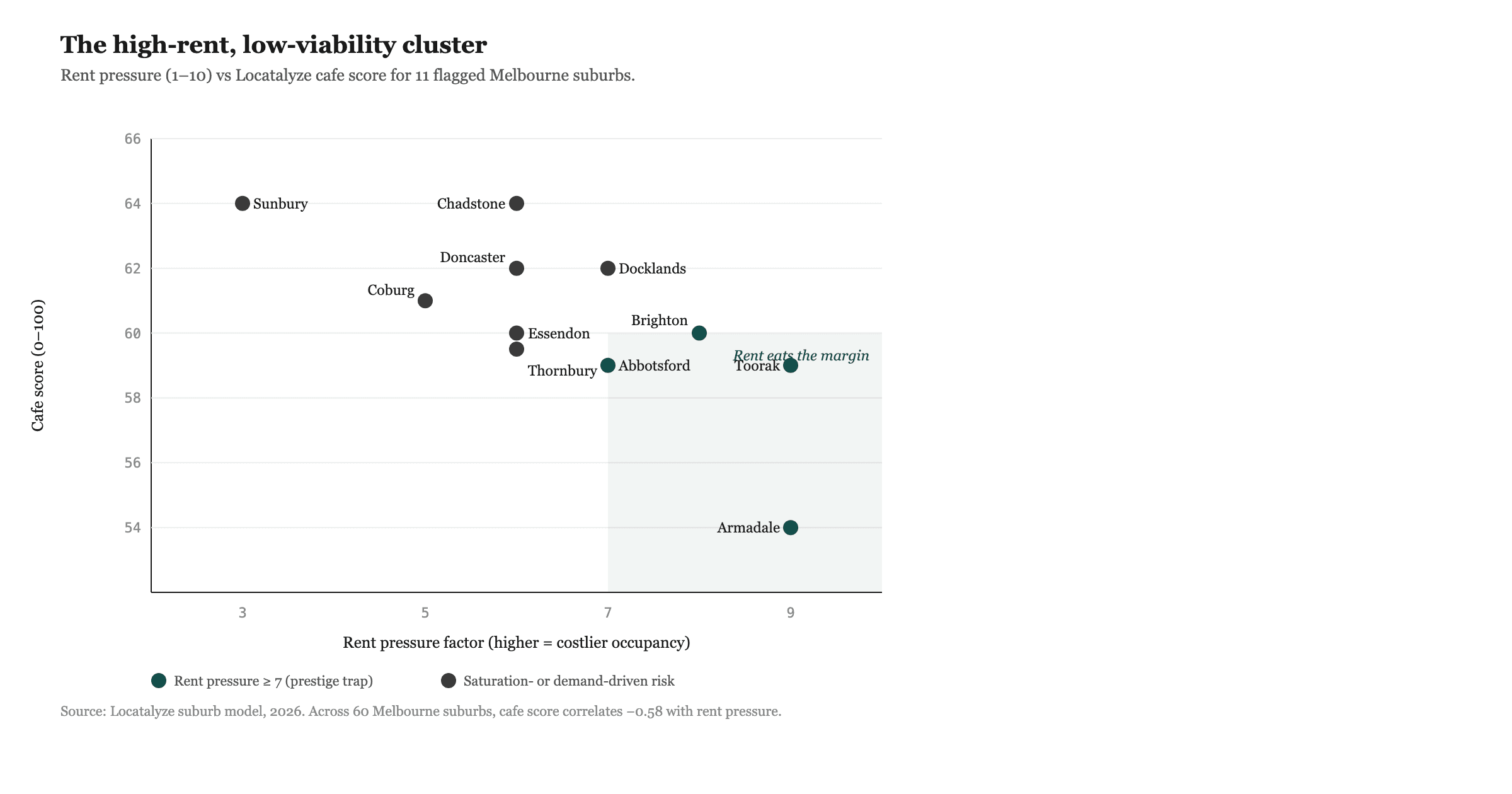

The high-ratio plays are Preston, Footscray, Box Hill and Brunswick. Each pairs strong demand (8 or 9) with the lowest tier of rent pressure (3 or 4), and the model rewards that pairing above the prestige inner suburbs that score similar demand at materially higher rent pressure (Locatalyze suburb model, 2026). Figure 2 plots the whole field on those two axes, and the pattern is hard to miss: the best risk-adjusted suburbs cluster in the upper-left — high demand, low rent — while the trophy postcodes drift right into the pay-to-play zone.

The ratio wins for a structural reason: rent is fixed by the lease and revenue is capped by the catchment. A Preston cafe at rent pressure 3 and demand 8 has slack in its rent-to-revenue arithmetic; gross effective rent lands at a share of turnover the business can absorb. A South Yarra cafe at rent pressure 7 and demand 10 trades more dollars but hands a larger share of them back as rent, and any softening in trade pushes the ratio into the danger zone faster. The prestige suburb is not a worse place to drink coffee. It is a worse place to underwrite a thin-margin business, because it offers less room for error against the same punishing failure base rate (ASIC, FY2023–24; Tourism Research Australia, June 2019 to 2024). The first-time operator's instinct is to chase the demand 10. The model says chase the ratio.

Top three versus bottom three, on the same metrics

To make the spread concrete, set the top three of this ranking against the bottom three on identical factors. The top three are Fitzroy, Brunswick and Preston. The bottom three of the fourteen-suburb GO field are Collingwood, Hawthorn and St Kilda.

All values: Locatalyze suburb model, 2026.

The gap between top and bottom is eight cafe-score points, and Figure 3 shows where those points come from. It is not demand — the bottom three average a demand reading barely below the top three. The separation is rent pressure and competition. Fitzroy's competition reading of 3 and Preston's rent pressure of 3 are what lift them; Collingwood's competition of 6 and St Kilda's rent pressure of 6 are what hold them back. Same city, similar demand, very different odds — and the difference is exactly the two cost-side factors the failure data keeps flagging (ASIC, FY2023–24).

Reading rent and foot traffic honestly in Melbourne

Two pieces of local context keep this ranking grounded rather than abstract.

On rent, Melbourne's super-prime CBD retail was last benchmarked at roughly $6,250 per square metre per annum, a figure that had fallen 7.4% quarter on quarter and 13.8% year on year at the time of measurement (CBRE, *Australian Retail Figures*, reported 2023). That is the trophy-frontage number, not the suburban-strip number, and the gap between the two is the entire reason the rent-pressure factor exists. A Fitzroy or Brunswick strip tenancy trades at a fraction of CBD super-prime, but the discipline is the same: take the gross effective rent — base rent plus outgoings, net of any incentive amortised over the term — and test it against the revenue the catchment can realistically produce, not the revenue the agent implies. The suburbs that win this ranking win because that test passes with room to spare. For how lease costs actually move across markets and formats, the analysis of commercial rent per square metre across Australia is the companion read.

On foot traffic, Melbourne is unusual in that the data is genuinely public. The City of Melbourne runs an automated Pedestrian Counting System of street sensors that record multi-directional movements 24 hours a day, every day, with the counts published openly. It is a better dataset than almost any operator has for their own strip — and it still does not tell you what you need. A high pedestrian count is a revenue *ceiling*, not a revenue *forecast*. A cafe converts a small, fairly stable fraction of the people who pass, and that fraction depends on format, price point and the daypart mix the location supports. Bourke Street Mall posts enormous counts and remains a difficult cafe proposition, because the rent has fully capitalised the footfall and the competition is dense. This is the trap the thesis names: foot traffic is the input the market has already priced. The framework for translating it into a defensible site decision sits in the retail site selection metrics that move a decision from a single headline number to a system.

What this ranking does not tell you

The honest limitations matter as much as the rankings.

It is a suburb-level model, not a shopfront model. A suburb score is a base rate for the area; your specific corner can sit well above or well below it. A Preston cafe on the wrong side of a quiet block can underperform the suburb's 78, and a Carlton cafe on a prime Lygon Street corner can beat the suburb's 75. The score narrows the search. It does not pick the lease.

It does not benchmark your actual rent. The model reads rent *pressure* — the local market's tendency to price hard against achievable revenue — not the dollar figure on the lease you are negotiating. Two tenancies in the same suburb can carry very different gross effective rents depending on frontage, incentive and term. The factor tells you the climate; it cannot read your contract.

It does not capture operator quality, capital structure or timing. A well-located cafe run badly still fails, and the model isolates none of management skill, food quality or marketing. Nor does it know your capitalisation runway — the eighteen-month wall that the failure data describes is decided as much by how thinly you funded the fitout as by the suburb you chose (Tourism Research Australia, June 2019 to 2024). And suburb dynamics move; a competition reading of 4 today can be a 6 in two years if a strip gentrifies fast.

It does not predict individual outcomes. The base rate in Australian hospitality is roughly 46% closure over four years, and the second-highest corporate insolvency share of any sector (Tourism Research Australia, June 2019 to 2024; ASIC, FY2023–24). A high suburb score moves you toward the better tail of that distribution. It does not exempt you from it. The full breakdown of how those base rates actually behave is in the Australian cafe failure rate analysis, and the inverse of this ranking — the Melbourne suburbs where cafes most often fail — is the other half of the same picture and worth reading alongside it.

Shortlisted a suburb? Check a specific café address.

Suburb demand is a base rate. Screen the exact shopfront for competition, catchment and rent pressure before you commit. Category is prefilled as café — you still choose the address.

Analyse a café address freeWhat this means before you sign a lease

The practical implication is that the suburb shortlist is the start of the work, not the end of it. This ranking tells you where the demand-to-rent-to-competition ratio still works in Melbourne in 2026: Fitzroy at the top, then the high-ratio cluster of Brunswick, Preston, Footscray and Box Hill, then the solid-but-pricier inner suburbs where you pay more of your trade back as rent. It tells you to be sceptical of the trophy frontage, the tourism-dependent strip and the saturated prestige postcode, however good they look at 8am on a Saturday.

What it cannot do from a suburb average is price your actual corner. Two doors apart on the same Brunswick street can be different businesses — different walk-past, different gross effective rent, different competition inside the 500-metre catchment. That is the gap between a suburb score and a site decision, and it is exactly the gap a single-address analysis closes. The same logic extends across formats and cities through the broader location analysis platform, and if you are weighing Melbourne against the west, the best Perth suburbs for a first cafe applies this same five-factor model to a very different market.

Shortlisted a suburb? Check a specific café address.

Before you commit, see the footfall, competition and rent-fit picture for the specific shopfront — not the suburb mean. Free to start; modelled financials stay optional.

Analyse a café address freeThe 54% of Melbourne cafes that will still be trading in four years are not the ones who chased the busiest footpath. They are the ones who found the suburb where the ratio worked, then proved the specific site carried its rent before they signed. Start with the suburb. Finish with the address.

References

Australian Securities and Investments Commission, *Annual insolvency data, FY2023–24* (25 July 2024): Accommodation and Food Services the second-largest source of corporate insolvency, 15% of all external administrations, behind Construction at 27%; more than 11,000 companies entered external administration in FY24, up 39% year on year. asic.gov.au

Tourism Research Australia, *Tourism Businesses in Australia: June 2019 to 2024* (built on ABS Counts of Australian Businesses): 54% of cafes, restaurants and takeaway businesses operating in June 2020 were still operating in June 2024, among the lowest of any category, against 64% for all Australian businesses. tra.gov.au

Australian Bureau of Statistics, *Counts of Australian Businesses, including Entries and Exits*: underlying business-survival and counts data on which the four-year survival figures are built. abs.gov.au

City of Melbourne, *Pedestrian Counting System*: automated network of street sensors recording multi-directional pedestrian movements 24 hours a day, with hourly counts published as open data. melbourne.vic.gov.au

CBRE, *Australian Retail Figures* (reported 2023): Melbourne super-prime CBD retail net face rent of approximately $6,250 per square metre per annum, down 7.4% quarter on quarter and 13.8% year on year at the time of measurement. cbre.com.au

Locatalyze suburb model, 2026: cafe scores, composite scores, verdicts and the five-factor demand, rent pressure, competition, seasonality and tourism readings for 60 Melbourne suburbs. Cafe score correlates with rent pressure at −0.58 (strongest single driver) and demand at +0.49 across the Melbourne set.

How to use this guide before shortlisting

- 1

Shortlist 2–3 suburbs that match your format (local regulars vs destination brunch).

- 2

Pin exact shopfronts — suburb scores hide bad corners and overpriced strips.

- 3

Compare rent offers against projected covers, not against “average Melbourne café rent”.

- 4

Walk each shortlist at peak and trough before you pay a deposit.

Related: see our Melbourne failure patterns in Melbourne suburbs where new cafés fail, and methodology for how Locatalyze scores competition and rent.

Related reading

Frequently asked questions

About the author

Locatalyze Research Team

Location intelligence, Locatalyze

The Locatalyze research team builds the location-scoring models behind the platform and writes up what the data shows for Australian operators.

Tools first — then a full report for your address

Free rent, viability, and break-even checks. Upgrade when you are ready for competitors, map, and numbers for a specific site.

No signup required for tools