Commercial rent per square metre across Australian capitals: a 2026 operator's reference

Locatalyze Research Team

Location intelligence, Locatalyze

The most expensive shopfront rent in the country sits on Pitt Street Mall in Sydney, at roughly US$795 per square foot per annum, up about 4% on the year (Cushman & Wakefield, "Main Streets Across the World 2025", Nov 2025). Translate that into the units a tenant actually signs against and it lands somewhere near AUD $12,000 per square metre per year for the best frontage on the best pedestrian strip in Australia. Now picture a 90 sqm strip shopfront three suburbs out, the kind a café or a homewares store actually takes. The Pitt Street number tells you almost nothing about what that lease will cost. It is a record-holder's figure, quoted because it is extreme, and it gets recycled every November as if it described the market. It does not.

Key takeaways

2026 data honesty note

Public capital-city retail face rents still lag behind broker research desks. The CBRE Q2 2023 super-prime CBD figures cited below remain the cleanest open city-by-city anchors — and they are outdated for signing. Use them only to sanity-check order-of-magnitude quotes, then refresh with current agent comps, REA/commercial listings, and your solicitor’s review of the offer.

This is the problem with "commercial rent per sqm Australia" as a search. People want a tidy table: city down the side, format across the top, a dollar figure in every cell. That table exists. It is built every quarter by valuers and by the research desks at CBRE, JLL, Colliers and Knight Frank. It is also, almost entirely, behind a paywall or inside a gated PDF, and the few numbers that leak into the open are either super-prime outliers or years old. An operator looking at a 60–120 sqm site has to make peace with that gap before anything else, because the gap is the real subject here.

So this reference does two honest things. It lays out the small set of per-sqm figures that are genuinely public and sourced, with their dates and their caveats attached. And it explains why the headline dollar-per-metre figure is the least useful number in a lease anyway. What you are actually trying to solve for is gross effective rent — face rent adjusted for the incentive, with outgoings and promotional levies folded in, expressed per square metre of lettable area you can actually trade from. The public anchors do not give you that number. They bracket it. Used properly, they tell you whether a quoted rent is plausible for the city and the format, and they tell you when a landlord's agent is quoting you a super-prime rate for a secondary site. That is worth having. A precise per-sqm table for your exact street is not something the open internet will give you, and any source that claims otherwise is guessing.

The four numbers that are actually public

Start with what can be cited without inventing anything. The cleanest specific figures in the open are CBRE's super-prime CBD retail net face rents from the second quarter of 2023: Sydney at $10,944/sqm, up 1.5% on the quarter; Melbourne at $6,250/sqm, down 7.4% on the quarter; Brisbane at $3,595/sqm, up 7.2%; and Adelaide at $3,275/sqm, up 7.4% (CBRE, Australian Retail Figures, Q2 2023). Those four sit in the figure above.

Read the label carefully, because every word in it is load-bearing. "Super-prime" means the single best space in the CBD core, not an average and not your site. "CBD" excludes the suburban strips and the shopping centres where most 60–120 sqm operators actually trade. "Net face" means the headline rent before any incentive, with outgoings charged separately on top. And "Q2 2023" means these numbers are heading toward three years old. CBRE's own later commentary notes that super-prime CBD was the one retail sector that did not grow in Q4 2024, while Perth super-prime CBD net face rose 3.7% year-on-year to the end of 2024 (CBRE, 2025 retail rent dynamics). That implies the 2023 Sydney, Brisbane and Adelaide levels are broadly still in the neighbourhood, perhaps slightly higher, but "broadly in the neighbourhood" is not a figure you sign a lease against. Treat the four numbers as a 2023 snapshot that must be refreshed before reuse. The `lastDataRefresh` on this page is 2026-05-31; the underlying CBRE values are not.

That is the extent of the city-by-city, dollar-specific public record for CBD super-prime. For Pitt Street Mall there is the Cushman & Wakefield high-street figure already mentioned, which is a headline prime rent for the best space on that one street and was reported up 4% on the year (Cushman & Wakefield, "Main Streets Across the World 2025", Nov 2025). Bourke Street Mall in Melbourne ranks second-dearest in the country in the same survey, but no current dollar figure for it was openly published that could be confirmed.

Then the data runs out. For Perth and Canberra, CBRE's Q2 2023 release described super-prime CBD as "stable" and disclosed no dollar figure. For Newcastle, the Gold Coast, Wollongong, Hobart and Darwin, no openly published, authoritative per-sqm retail figure could be found at all. For shopping-centre formats — regional, sub-regional, neighbourhood — and for suburban strip retail across every city, the same applies: the per-sqm benchmarks exist inside the research houses' subscriber products and valuers' files, and they are not in the open. Stating that plainly is more useful than filling the cells with numbers scraped from a 2011 or 2018 report, which is where most of the "average commercial rent" content online quietly gets its figures.

Why the table has holes, and why that is the honest answer

The holes are not an accident of searching badly. They are structural. Retail rent benchmarks are the product the research houses sell. CBRE's Australian Retail Figures, Colliers' retail snapshots, JLL's market dynamics and Knight Frank's Australian Retail Review are commercial assets, released as gated PDFs or JavaScript-rendered dashboards, with the granular per-sqm tables reserved for clients. The directional headlines get a press run; the matrix does not. On top of that sits the valuation profession, where a registered valuer assembles comparable lease evidence — recent deals on similar space nearby, adjusted for incentive, term and condition — to produce a rent opinion for a specific property. That evidence is confidential to the parties. There is no public registry of what the shop two doors down actually agreed to pay net of its fitout contribution.

So when a page promises you "average retail rent per square metre" for, say, Newcastle or the Gold Coast, ask where the number came from. Usually it traces back to a stale report, a listing portal's asking rents (which are face rents before negotiation and systematically overstate what gets signed), or pure interpolation between two cities. None of those is a benchmark. An asking rent is an opening bid. A benchmark is settled evidence. The difference matters most precisely where data is thinnest, because that is where a confident-sounding wrong number does the most damage to a 90 sqm tenant with one shot at the lease.

The directional public signals are worth holding lightly. Colliers put national retail face rents up about 1.5% year-on-year in Q2 2025 and flagged that new retail floor-space supply is set to fall roughly 72% over five years, with strong competition for prime, high-footfall sites (Colliers, Australian Retail Snapshot, Q2 2025). CBRE separately noted city-centre rents up about 4% since 2022 on competition for prime locations (CBRE, 2025 retail rent dynamics). Read those as direction and pressure, not as levels. They tell you the prime end is tightening and that supply is not coming to rescue you. They do not tell you what your strip will cost.

What the dollar-per-metre figure leaves out

Here is the argument the rest of this piece rests on. Suppose a landlord's agent quotes you $900/sqm for a 90 sqm shop. That is a face rent: $81,000 a year headline. It is also nearly meaningless on its own, because four things sit between that number and what leaves your account.

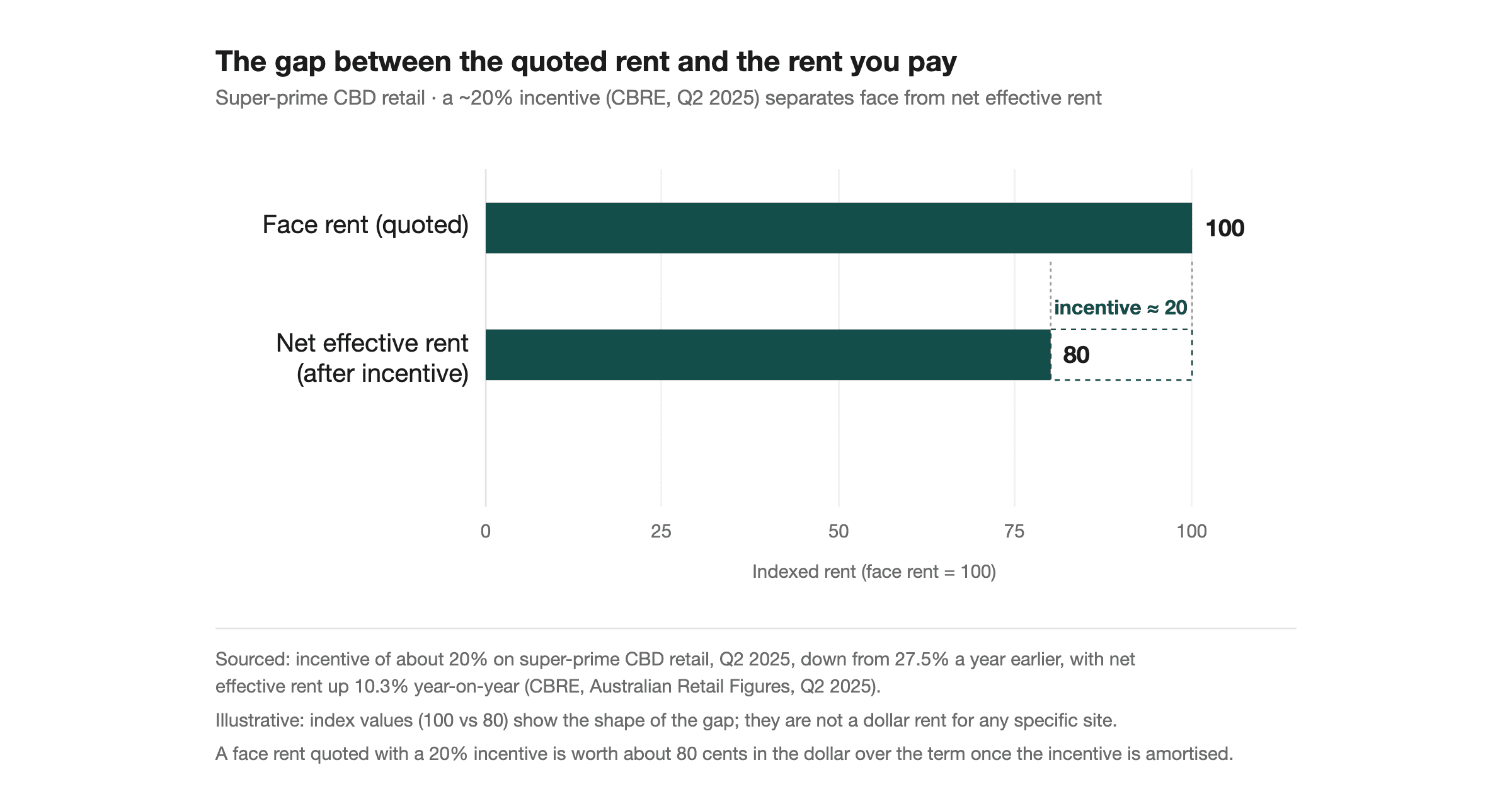

The first is the structure — gross or net. Under a gross lease, the rent figure includes the building outgoings: council rates, water, insurance, common-area maintenance, the body corporate or management levy. Under a net lease, you pay those outgoings on top of the rent, and in retail they routinely add $100–$250/sqm or more depending on the building. The same "$900/sqm" is a materially different commitment depending on which one you are being quoted. Always ask, and always get the outgoings schedule in writing before you compare two sites.

The second is the incentive. In a soft or competitive leasing market, landlords hold the face rent high — it protects the building's valuation — and discount through incentives instead: rent-free periods, a fitout contribution, a capped rent for the early months. CBRE reported super-prime Sydney CBD incentives around 17% in the first half of 2025, up from about 13% a year earlier. An incentive of that size changes the economics entirely. A $900/sqm face rent with a 20% incentive over a five-year term is, in cash terms, closer to $720/sqm. The face rent is the number that goes in the lease and the press release. The incentive is the number that decides whether you can trade.

The third is the distinction between face and effective rent. Gross face rent is the headline including outgoings. Net face rent is the headline excluding them. Gross effective rent is the figure you actually want: the total occupancy cost — rent plus outgoings plus promotional levy — averaged over the lease term after the incentive is spread across it, per square metre. That single number is what lets you compare a CBD net-face quote against a strip gross quote against a centre deal with a turnover-rent clause. It is also the number no public table gives you, because it depends on the specific incentive and outgoings you negotiate.

The fourth is lettable area itself. Per-sqm only means something against a defined area, and retail areas are measured to a standard (broadly, the Property Council's method) that may or may not match the floor you think you are renting. Verify the lettable area in the lease against a measured plan. A few square metres of difference on a small shop moves your effective rate enough to matter.

Put those together and the implication is blunt: two shops quoted at the same $/sqm face rent can carry occupancy costs 30–40% apart once structure, incentive and outgoings are settled. The per-sqm headline is the start of the conversation, not the answer.

Reading the Pitt Street figure against a real shopfront

Take the one super-prime anchor and use it the way an operator should — as a ceiling and a sanity check, never as a comparable. Pitt Street Mall at roughly AUD $12,000/sqm headline (Cushman & Wakefield, "Main Streets Across the World 2025", Nov 2025) is the most expensive retail frontage in Australia. It exists because the foot traffic past those doors is among the densest in the country and the international flagship brands that want it will outbid any independent operator. No café, no boutique, no service business taking 60–120 sqm is competing for that space or anything like its rate.

What the anchor does give you is scale. The CBRE Q2 2023 set shows Sydney super-prime CBD net face at $10,944/sqm and Adelaide at $3,275/sqm — a 3.3x spread between two capital-city cores for equivalent best-in-class space (CBRE, Australian Retail Figures, Q2 2023). That spread is the useful intelligence. It tells you that "prime retail rent" is not a national figure; it is a deeply local one, and the same business model carries wildly different occupancy costs depending on the city and, far more, the precinct. A rate that is aggressive in Adelaide's core would be a bargain on Pitt Street and a rip-off on a quiet suburban strip.

So when an agent on a secondary strip quotes you a rate, the question is not "is this below Pitt Street" — everything is below Pitt Street. The question is whether the rate is consistent with the footfall and the trade area the site actually commands, and whether the effective rent, after incentive and outgoings, lets your forecast revenue carry it. That is a site-level question, and it is answered with site-level evidence: counted foot traffic, the real catchment, the competitor set, and comparable deals nearby. The national anchors cannot answer it. They only stop you mistaking a secondary site quoted at a prime rate for a fair deal. If you want to see how footfall translates into trade for a small shopfront, the mechanics are worth a read in our note on how foot-traffic data feeds a hospitality forecast, and the survival maths behind café occupancy costs sits in our analysis of why so many Australian cafés close.

A cross-city reference, with the gaps shown honestly

Below is the comparison table this kind of piece is supposed to contain. It is built only from figures that could be opened and sourced. Empty cells are marked, not filled. The honesty of the empty cells is the point: this is the actual public record, not a manufactured one.

Provenance: the four CBD super-prime dollar figures are CBRE's Australian Retail Figures for Q2 2023, net face rent, quoted via that release; they are 2023 values and must be refreshed before any current use. The Sydney high-street figure is an indicative AUD conversion of Cushman & Wakefield's November 2025 Pitt Street Mall headline rent. "Not publicly published" means no authoritative per-sqm figure for that city-and-format could be opened from a research house or public dataset as at 2026-05-31; the data exists inside proprietary products and valuers' files, not in the open. Do not read an empty cell as "cheap" or "unknowable" — read it as "priced privately, obtainable only through a valuation or a research subscription".

What this reference does not cover, and where it stops

This is a public-anchor reference, and its limits should be stated as plainly as its figures. It does not give you strip or neighbourhood-centre per-sqm rents for any city, because those are not openly published. It does not give you a current Melbourne, Brisbane or Adelaide CBD figure — only the 2023 super-prime values. It does not cover Perth, Canberra, Newcastle, the Gold Coast, Wollongong, Hobart or Darwin with a dollar figure, because none was available. It says nothing reliable about turnover-rent clauses, percentage rent thresholds, ratchet provisions or make-good obligations, all of which can swing the real cost of a retail lease as hard as the headline rent does. It does not substitute for a valuation, and it cannot tell you what your specific site is worth. Treat it as the bracket, not the answer, and treat every dated figure in it as something to re-source before you act on it.

How to actually price a site

The workflow that follows from all of this is short and unglamorous. Get the face rent and the structure first — gross or net, and the full outgoings schedule in writing, because a net quote without its outgoings number is not a quote. Find out the incentive on offer; in the current market a prime or near-prime site without an incentive is the exception, and the incentive is where the real negotiation lives. Convert everything to one gross effective rent per square metre of verified lettable area, spreading the incentive across the term, so you can compare unlike sites on a single number. Stress that effective rent against a revenue forecast built from the site's actual footfall and catchment, not from a city average. Then benchmark the quote against the public anchors in this piece: if a secondary strip is being quoted near a capital-city super-prime rate, that is a flag, not a fair price.

For a site you are serious about, pay for a valuation or a short leasing-advisory engagement. A registered valuer or a tenant-rep agent has the comparable lease evidence that the open internet structurally cannot, and on a five-year commitment the fee is trivial against the risk of overpaying by 20% for a decade. Use the public figures to know roughly where the ceiling is and to catch an obviously inflated quote; use paid, site-specific evidence to settle the actual number.

For the catchment and footfall side of that forecast — the part the rent has to be carried by — that is what Locatalyze is built for. You can run a free location read by entering an address and seeing the trade area, competitors and demand signals before you commit, or start a full location analysis. City-specific reads for Sydney sites, Melbourne sites and Brisbane sites fold the local competitive and demand picture into the same view. The rent number you negotiate is only as good as the revenue you can prove the site will carry, and that is the figure worth getting right.

The rent you negotiate is only as good as the revenue the site can prove it will carry — so read the trade area, competitors and demand signals before you sign.

Free location score, map, data confidence and PROCEED / VERIFY / AVOID recommendation. Modelled financials stay optional.

Analyse your addressReferences

Cushman & Wakefield, *Main Streets Across the World 2025*, November 2025. Pitt Street Mall headline retail rent ~US$795/sf/yr (~€7,294/sqm), up ~4% y/y. cushmanwakefield.com

CBRE, *Australian Retail Figures, Q2 2023*. Super-prime CBD retail net face rents: Sydney $10,944/sqm, Melbourne $6,250/sqm, Brisbane $3,595/sqm, Adelaide $3,275/sqm. cbre.com.au

CBRE, 2025 retail rent dynamics and CBD vacancy releases (H1/H2 2025; Q4 2024 commentary). City-centre rents up ~4% since 2022; super-prime CBD the only sector not to grow in Q4 2024; Perth super-prime +3.7% y/y to end-2024; Sydney super-prime incentives ~17% in H1 2025. cbre.com.au

Colliers, *Australian Retail Snapshot, Q2 2025*. National retail face rents +1.5% y/y; new retail floor-space supply set to fall ~72% over five years. colliers.com.au

Knight Frank, *Australian Retail Review*, April and September 2025. Macro and investment context; no per-sqm shopfront benchmark table published. knightfrank.com.au

Australian Bureau of Statistics — retail and economic context. abs.gov.au

*Data note: the CBRE per-sqm figures in this reference are Q2 2023 values and the most recent specific CBD figures that could be sourced in the open. They must be refreshed before being relied on for a current decision. Last data review: 2026-05-31.*

Before you sign: rent verification checklist

- 1

Get face rent, outgoings estimate, promotional levy, and any fit-out contribution in one written schedule.

- 2

Confirm whether area is GLAR / NLA and whether back-of-house counts toward rentable metres.

- 3

Ask for three recent comparable deals on the same strip (even if redacted) — not CBD mall headlines.

- 4

Model break-even on your ticket size and covers; if rent needs heroic volume, the site is wrong or the rent is.

- 5

Walk peak and off-peak trading hours before you accept “high foot traffic” as justification for premium rent.

Common mistakes with rent benchmarks

Related reading

Frequently asked questions

About the author

Locatalyze Research Team

Location intelligence, Locatalyze

The Locatalyze research team builds the location-scoring models behind the platform and writes up what the data shows for Australian operators.

Tools first — then a full report for your address

Free rent, viability, and break-even checks. Upgrade when you are ready for competitors, map, and numbers for a specific site.

No signup required for tools