West End Brisbane in 2026: The Food Suburb That's Finally Ready — But Only for the Right Format

Founder, Locatalyze

West End has occupied a specific position in Brisbane hospitality conversations for the better part of fifteen years: the suburb that's about to arrive. The food culture has been genuine for longer than its commercial infrastructure has been able to support. The demographic has been transitioning — from a historically low-income, diverse residential catchment toward a younger professional renter population — at a pace that has been visible but frustratingly gradual for operators who committed early. In 2026, something has shifted. The apartment development cycle that began six to eight years ago is now delivering residents. The median income of West End's catchment has moved materially. The price point ceiling that constrained operators for years has lifted to a point where previously unviable formats are becoming commercially feasible. But — and this is the part that the "West End is ready" narrative glosses over — not all formats, not at all rents, and not across the entire suburb uniformly. This is a granular analysis of where West End actually is in 2026, what the numbers show, and which specific opportunities have genuinely opened up versus which ones are still 2–3 years away.

What Has Actually Changed in West End (2020–2026)

The most important single change in West End's commercial food and beverage environment over the past six years is the delivery of approximately 2,400 new residential dwellings in medium-to-high-density apartment projects within the suburb's core catchment. This isn't projected supply — it's completed supply, with residents in occupation, spending locally.

The demographic profile of these new residents is meaningfully different from West End's historical baseline. The new apartment stock has attracted primarily professional couples and singles in the 28–42 age range with household incomes in the $88,000–$125,000 band. This demographic has a demonstrably different dining spend pattern from the lower-income renters and long-term residents who previously dominated the catchment. They eat out more frequently, spend more per occasion, and are more willing to patronise concepts at the $35–$55 per head dinner price point that had been commercially difficult in West End for years.

2,400+

New residential dwellings delivered in West End's core catchment 2018–2025

$88k–$125k

Household income range of dominant new resident demographic in new apartment stock

$3.2k–$5.4k

Current all-in weekly rent range for food and beverage on Boundary Street

The Boundary Street Breakdown

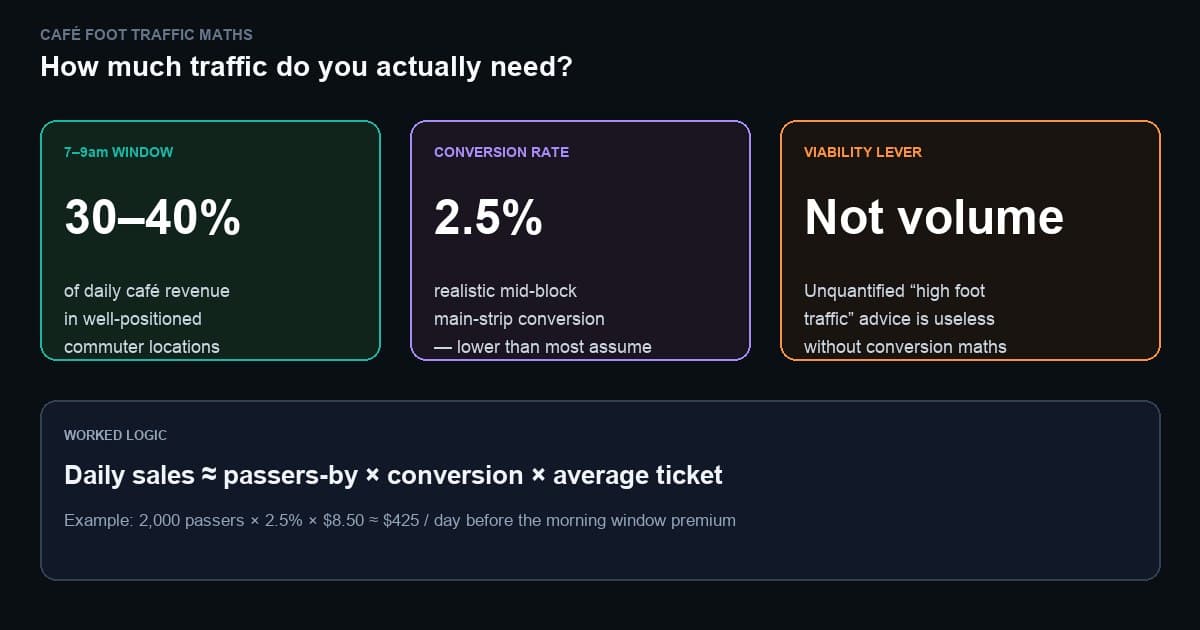

Boundary Street is West End's primary commercial and hospitality spine, but like most established food streets in Australian inner suburbs, its commercial characteristics vary significantly along its length. The section between Browning Street and Russell Street captures the highest foot traffic and the most active hospitality cluster. North and south of this core zone, foot traffic drops and the precinct character transitions.

The Browning-to-Russell section now generates 9,000–14,000 daily pedestrians on an active trading day — a meaningful increase from the 6,000–9,000 that characterised the same section five years ago, driven by the new residential density feeding into the strip. Saturday morning peaks at 13,000–18,000. These numbers support the café and casual dining formats that have always been West End's natural format fit — and at the current rent levels, the unit economics are achievable in ways they weren't when the demographic was thinner.

The Formats That Work Now — Specifically

Specialty café with strong brunch: this is West End's most commercially validated format type in 2026. The new residential demographic is a heavy weekend brunch consumer, the established food culture means customers are quality-literate (a good product will generate loyalty faster here than in less food-aware markets), and the rent levels relative to revenue potential are more favourable than comparable inner-Brisbane positions. Operators who can generate $3,200–$4,000 per week in all-in rent and hit $18,000–$24,000 weekly revenue are building viable businesses here.

Mid-range casual dinner at $38–$52 per head: this is the category where the demographic shift has created the most genuine new opportunity. West End has traditionally had limited mid-range dinner options — the corridor has skewed toward cheap-and-cheerful (served by the established multicultural operators who pre-date the demographic shift) or toward premium concepts that were ahead of the market. The $38–$52 per head casual dinner segment has limited strong established competition and a demographic that is actively looking for it. This is the specific opportunity that the 2026 version of West End offers that the 2020 version did not.

What's Still Not Ready

Fine dining above $70 per head: the West End catchment has grown meaningfully but is not yet deep enough to sustain a premium concept that depends on high repeat visitation at $70+ per head. The density of households in the target income bracket for regular premium dining is insufficient relative to what a viable fine dining business requires. This will change — the development pipeline suggests continued residential densification at middle-to-upper income levels — but it is not there in 2026.

Fashion-led premium concepts (expensive fit-outs, editorial brand positioning, high marketing expenditure): West End's food culture values authenticity and quality over aesthetics and brand. The operators who have succeeded here with premium positioning have done so through food and hospitality quality, not through expensive brand investment. Operators who invest $200,000+ in a fit-out and brand build to signal premium in West End are misreading the market — the demographic will support the price point if the substance is there, but it will not support the price point simply because the aesthetic is expensive.

The 2026 West End opportunity window

The demographic has arrived sufficiently to support mid-range casual concepts that were previously unviable. The rents have not yet fully caught up with this demographic shift. This gap — between current demographic capacity and current rent levels — is the commercial opportunity. It will narrow as landlords update their rent expectations over the next 12–24 months. Operators who enter now, at current rent levels, with formats calibrated to the current demographic, are entering at the most favourable point in the market cycle West End has offered.

Locatalyze covers every West End address with current demographic profiling, competitive mapping, and rent benchmarking updated for 2026 market conditions.

Free location score, map, data confidence and PROCEED / VERIFY / AVOID recommendation. Modelled financials stay optional.

Analyse my West End locationRelated reading

About the author

Prashant GuleriaFounder, Locatalyze

Prashant built Locatalyze to replace suburb mythology with commercial data — especially in growth markets where timing is everything.

Tools first — then a full report for your address

Free rent, viability, and break-even checks. Upgrade when you are ready for competitors, map, and numbers for a specific site.

No signup required for tools