The Suburb That Killed Three Great Restaurants — And Why the Fourth One Finally Made It

Founder, Locatalyze

In inner Melbourne, there's a suburb that hospitality insiders have watched with a mixture of fascination and sadness for the better part of four years. The suburb has everything that should work: growing residential population, increasing average incomes, street-level activity, a demographic that theoretically loves to eat out. And in the main restaurant strip, there have been three serious, well-funded, genuinely talented operators who looked at those indicators and committed. The first: a modern Asian diner with genuine food credentials, a well-regarded team, $280,000 fit-out. Closed after 19 months. The second: a neighbourhood Italian concept with a small-plates format, press coverage at opening, a following from the chef's previous job. Closed after 26 months. The third: a wine-bar-led concept with serious provenance in the bottle list and a bistro menu that the food press respected. Closed after 14 months — the shortest run of the three, and the most painful, because by then the pattern was visible and the third operator had watched two predecessors fail without drawing the right conclusions from what they'd seen. The fourth operator opened 11 months ago. The business is profitable. The waitlist on Friday and Saturday nights has been consistent since month four. Here is the complete story of what was different.

What Made the Suburb Look So Attractive (And Why That Was the Problem)

The suburb had a genuine story. Average household incomes had been increasing meaningfully for four consecutive years. The residential population was growing through apartment development. Younger professional renters were moving in alongside established owner-occupier households. New retail — independent bookshops, boutique homeware, specialty coffee — was appearing on the main strip. By every qualitative indicator, the suburb was on a trajectory that suggested it was becoming the kind of area that supports mid-range to premium food and beverage.

Every operator who committed to the strip before the fourth one was looking at the same story and drawing the same conclusion: this area is ready, or nearly ready, for my format. The problem is that "nearly ready" and "ready" are separated by a gap that might be 18 months or 3 years, and in that gap lives the entire commercial fate of a business on a 5-year lease. The suburb's demographic story was real. Its timeline relative to each operator's business plan was not.

"This suburb is about to be ready for a concept like ours" is one of the most expensive sentences in Australian hospitality. The gap between "about to be ready" and "actually ready" typically runs 18 months to 3 years. In a 5-year lease, you have no margin for being early.

The Specific Failure Pattern of the First Three Operators

All three operators shared a specific pattern that became obvious in retrospect. They had assessed the suburb's demographic trajectory — correctly — and calibrated their format to the suburb's aspirational future demographic rather than its current one. This is a completely understandable error. The suburb's future demographic was their customer. The suburb's current demographic was not.

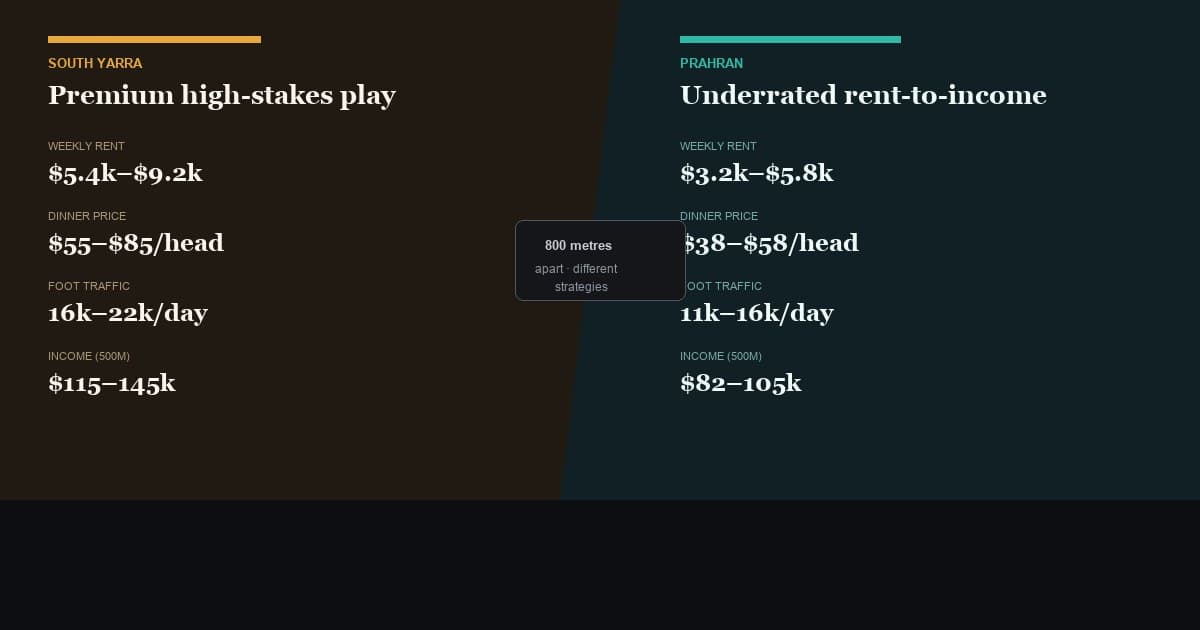

At the time each of the first three restaurants opened, the suburb's residential population was primarily composed of: established, longer-term owner-occupiers in the 50–65 age bracket with strong local identity but conservative dining-out habits; and younger renters (28–38 years, professional, share households) with genuine food culture but a household income profile that supported $22–$28 main courses more naturally than $38–$48.

The formats all three operators deployed — modern Asian at $45 mains, Italian small plates at $52 per head, wine-bar bistro at $55 per head — were calibrated for a demographic that was 18–36 months from arriving in sufficient density. The current catchment had the aspiration for these formats. It lacked the income concentration to sustain them at the covers required to cover operating costs.

What the Fourth Operator Did Differently: The Pre-Commitment Analysis

The fourth operator approached the location with a specific methodological difference from her three predecessors: she treated the current demographic as the operating reality and the future demographic as an upside scenario, not a baseline assumption. This is a subtle but consequential shift in how the business case was constructed.

She spent three weeks conducting the analysis that none of the previous operators had done in detail. Not because she was more diligent or more talented — she was operating from the advantage of having watched three failures and drawn the right conclusions from them. The analysis covered four specific areas.

Current spending patterns in the corridor

She visited every food and beverage business in the strip and the surrounding streets, at multiple times of day, across a full week. She noted approximate patronage levels, estimated average spend from menu prices and observable order patterns, and tried to understand which businesses were trading sustainably versus which were struggling. The picture was clear: the businesses trading well were operating at $22–$34 per head. A well-established café at $16 average transaction was consistently busy. A casual pizza and pasta concept at $28 mains had visible consistent patronage. An ambitious natural wine bar at $65 per head was clearly struggling — it had the third-most recent fit-out on the strip, suggesting it was one of the newer openings, and it was rarely more than 40% full during service.

The residential composition in granular detail

Not the suburb's median household income but the actual income distribution across the specific blocks within 800 metres of the address. Using ABS census data at the mesh block level, she mapped the proportion of households at different income quintiles. What she found: the suburb's rising median income was being driven by a small but growing cohort of high-income professionals in new apartment buildings, while the majority of existing residents sat in income quintiles that were compatible with $22–$34 main courses but not with $45–$55.

The 3-year development pipeline

She checked every DA lodgement within one kilometre over the previous 24 months. The development picture: two 80-unit apartment buildings approved and under construction, expected to complete in months 18–24 of her lease term. One of these buildings had a high proportion of 2-bedroom units priced above market average, suggesting a professional renter demographic. This was the specific demographic she needed — but it was 18–24 months away. Her business plan needed to be viable at current demographics with this development as upside, not as baseline.

The format that current demographics could sustain

Based on the preceding analysis, she built a unit economics model for three format options at different price points: a $38/head neighbourhood bistro (matching current demographics well), a $45/head mid-range concept (ahead of current demographics), and a $32/head accessible format (below the aspirational positioning she wanted). The model at $38/head worked with the current demographic. The model at $45/head required the new apartment demographic to materialise within 12 months to reach break-even — which she couldn't depend on. She chose $38/head.

The Numbers Eleven Months Later

The fourth operator's restaurant — a neighbourhood bistro format with $38 average mains, a considered but accessible wine list, and a fit-out that was warm but not trying to be editorial — has been profitable since month seven. Current weekly revenue: approximately $24,000. All-in weekly rent: $3,400. Rent-to-revenue ratio: 14.2% — above ideal but heading in the right direction as volume grows. Net monthly profit: approximately $14,000–$18,000 depending on the month.

More importantly, the first of the two new apartment buildings has recently commenced occupation. The operator is already seeing new regulars from the building — younger professionals with exactly the income profile and dining behaviour that the previous operators had been waiting for. Her existing business is profitable at the current demographic. The incoming demographic is incremental upside. She is precisely where each of the three previous operators hoped to be but never reached.

$38/head

The price point that matched current demographics (vs $45–55 for failed operators)

Month 7

When the fourth operator reached profitability

$14–18k

Current net monthly profit (vs average -$4,200/month for the three who failed)

The Lessons That Transfer to Any Growth-Area Decision

The specific suburb in this story isn't the point. The pattern is. And the pattern appears repeatedly across Australian cities in areas undergoing gentrification or demographic transition.

Lesson 1: The current demographic determines your viability. The future demographic determines your potential. Build your business case on the current demographic and treat the future demographic as upside. Any business plan that requires the future demographic to materialise within 12 months to reach break-even is a bet, not a plan.

Lesson 2: Look at what's actually sustaining in the corridor. The businesses that are trading well in a corridor — with visible consistent patronage, without the obvious signs of struggle — are providing direct evidence of what price points the current demographic will support. This evidence is available in every corridor you're considering. You just have to observe it deliberately rather than looking for confirmation of your preferred format.

Lesson 3: The development pipeline tells you the timing story. Approved DA applications for residential development within your catchment tell you specifically when and approximately how many units of your target demographic will arrive. Check the pipeline. Map the timing. Build it into your business plan as a named scenario rather than a vague hope.

Lesson 4: Price point is more adjustable than operators think. The third operator in this story had a concept very similar in spirit to the fourth operator's — neighbourhood, accessible, quality-driven. The critical difference was a $17 gap in average spend that put one format above the current demographic's natural price point and one within it. That $17 per head difference, across a week of covers, is the difference between a business that works now and one that works in two years.

The question that determines timing fit

For any growth-area location decision, ask this specific question: "If this suburb's demographic doesn't change at all in the next 24 months, does my business model still work at current trading conditions?" If the honest answer is no, you are making a demographic timing bet. Know that clearly before you commit. Calculate your runway if the demographic arrives 12 months late. 24 months late. Then decide whether the bet makes sense.

Before committing to any growth-area location, run it through Locatalyze — current demographic composition, income distribution at the catchment level, development pipeline, and price point viability analysis for any Australian address.

Free location score, map, data confidence and PROCEED / VERIFY / AVOID recommendation. Modelled financials stay optional.

Analyse your locationRelated reading

About the author

Prashant GuleriaFounder, Locatalyze

Prashant built Locatalyze to give Australian founders the data-driven framework that separates operators who get location timing right from those who are perpetually early.

Tools first — then a full report for your address

Free rent, viability, and break-even checks. Upgrade when you are ready for competitors, map, and numbers for a specific site.

No signup required for tools