Why Adelaide is Australia's Most Underrated Restaurant Market — And the Specific Risks Operators Still Miss

Founder, Locatalyze

Adelaide gets mentioned in national food media with increasing frequency and genuine respect. The restaurant scene has produced operators and concepts that would be commercially successful in any Australian market. The food culture is real, the wine culture is exceptional, and the demographic — disproportionately educated, with strong ties to the hospitality and arts industries — is sophisticated in its dining preferences. For an operator looking at entry costs, competitive landscape, and format-market fit, Adelaide's commercial environment offers something that Sydney and Melbourne genuinely cannot: viable unit economics at rents that don't require exceptional volume to justify. But Adelaide is also a smaller, more contained market than eastern-seaboard capitals, and the specific dynamics of its commercial geography — the Rundle Street corridor, the CBD's trading pattern, the balance between local regulars and the event-driven visitor economy — require specific understanding that operators who import strategies from larger markets without adaptation consistently fail to develop. This analysis gives you that understanding.

The Numbers That Make Adelaide Genuinely Attractive

The rent differential is the headline number and it's real. An operator paying $3,200 per week all-in on Rundle Street in Adelaide is paying 35–55% less than a comparable position in Surry Hills or Brunswick. At that rent level, the revenue requirement for a viable business model drops dramatically. A 60-seat casual dining concept at $44 average spend running 12 services per week at 70% occupancy generates approximately $29,000 per week. Against $3,200 all-in rent, that's an 11% rent ratio — tight but commercially viable in ways that the same concept against $6,200 Sydney rent simply is not.

The Market Size Constraint: The Variable Eastern Operators Underestimate

The risk in Adelaide that operators from Sydney and Melbourne consistently misjudge is market size. Adelaide's metropolitan population is approximately 1.4 million — roughly one-third of Sydney and Melbourne. The population of the primary dining catchment for Rundle Street and the adjacent East End is proportionally smaller. This has two specific commercial consequences.

First: total available market for any specific meal occasion and price point is smaller. A fine dining concept targeting high-income professionals who dine out for special occasions more than four times per year has a smaller potential customer pool in Adelaide than in Sydney. This doesn't make fine dining non-viable in Adelaide — several exceptional fine dining concepts operate successfully here — but it means the market saturates faster, the required repeat visitation rate from your loyal customer base is higher, and there is less room for multiple strong operators in any given category to coexist at premium price points.

Second: the market has long memory. Adelaide's dining community is genuinely interconnected. Word of mouth travels faster and more comprehensively in a smaller, more cohesive market. An operator who delivers consistently can build loyal advocacy more quickly than in Sydney or Melbourne. An operator who has a poor early period — inconsistent quality, service problems, the teething issues that are normal in any opening — finds those problems more durably embedded in the market's memory. The smaller market amplifies both positive and negative reputation signals faster.

The Adelaide word-of-mouth amplifier

In a city of 1.4 million where the dining community is closely networked, a strong opening month generates loyalty advocacy that spreads faster than in a 5-million person market. But the reverse is equally true: a difficult early period, a viral negative experience, or a service failure that would be forgotten in Sydney can circulate through Adelaide's food network quickly and durably. The consequence: opening standards in Adelaide need to be higher from day one, not built toward. The margin for an uncertain opening in a small market is narrower than operators from larger markets expect.

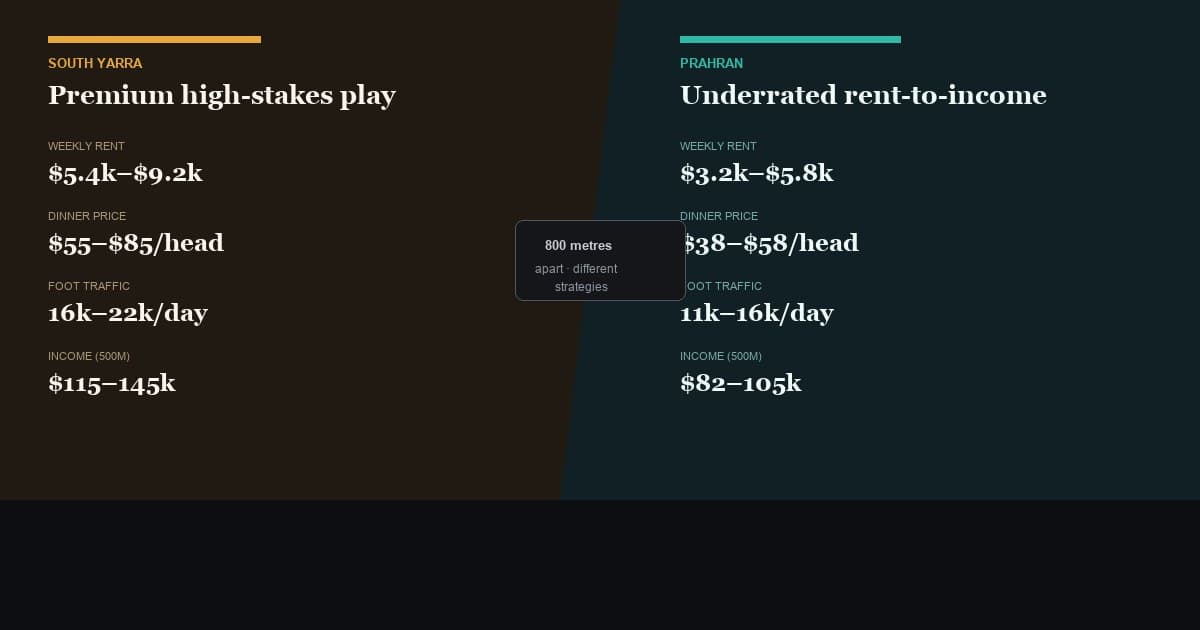

The Rundle Street Geography: East vs West

Rundle Street has a geographical split that operators must understand before committing to any specific position. The East End — from Pulteney Street eastward — has historically been the premium, destination-dining end of the strip. Lower foot traffic volume, higher quality of visit, a demographic that skews toward deliberate dining decisions rather than impulse choices. Restaurants on the East End of Rundle Street are destination operations — customers come because they chose to come, not because they happened to walk past.

The central and western sections of Rundle Street and the adjacent pedestrian mall generate higher foot traffic volume but a more mixed pedestrian profile that includes transit, retail, and entertainment traffic alongside dining-intent visitors. This section rewards formats that can capture impulse decisions — strong signage, accessible price points, quick service options — as well as considered dining.

The Adelaide commercial geography summary:

The Event Economy: Adelaide's Unique Revenue Amplifier

Adelaide's event calendar is a genuine commercial asset for food and beverage operators that has no direct equivalent in any other Australian market. The Adelaide Festival, Adelaide Fringe, WOMADelaide, Tasting Australia, and the Australian Formula 1 Grand Prix (in the Clipsal 500 era; now Adelaide 500) collectively create significant periods of above-average foot traffic and visitor dining spend that operators in other cities don't have access to.

The Adelaide Fringe alone — running for several weeks in February/March — generates significant incremental dining revenue for well-positioned operators in and around the East End and the Fringe precinct. Operators who deliberately position their concept to capture Fringe-adjacent dining (late kitchen hours, bar atmosphere compatible with post-show dining, proximity to major Fringe venues) consistently outperform their non-Fringe months during the festival period by 40–90%.

Modelling the event calendar explicitly into your annual revenue projection is not optional in Adelaide — it's a significant revenue planning variable. An operator who doesn't model Fringe season revenue as a separate scenario is leaving a meaningful planning input unaddressed.

$2.2k–$4.8k

All-in weekly rent on Rundle Street — 35–55% below comparable Sydney/Melbourne positions

+40–90%

Revenue uplift for well-positioned operators during Adelaide Fringe season

1.4M

Adelaide metropolitan population — the market size constraint eastern operators most often underestimate

The Honest Verdict: Adelaide Is Genuinely Worth Considering

Adelaide is not a consolation market for operators who can't afford Sydney or Melbourne. It is a market with genuine commercial advantages — lower entry costs, less competitive saturation in several categories, a food-literate demographic that is responsive to quality, and a wine culture that creates natural commercial synergy for concepts built around a serious drinks programme — that operators from eastern capitals consistently undervalue.

The operators who thrive in Adelaide are those who treat it as its own market with its own dynamics rather than a smaller version of Melbourne. The market size constraint is real and requires specific adaptation: tighter category targeting, higher opening standards, and more deliberate community marketing than the anonymity of a large city allows you to avoid. But the commercial fundamentals — rent-to-revenue ratios, competitive white space, demographic quality — are more favourable in Adelaide than anywhere else in Australia at comparable cultural sophistication levels.

Locatalyze covers every Adelaide address with rent benchmarking, competitive density analysis, demographic spend profiling, and event calendar revenue modelling.

Free location score, map, data confidence and PROCEED / VERIFY / AVOID recommendation. Modelled financials stay optional.

Analyse my Adelaide locationRelated reading

About the author

Prashant GuleriaFounder, Locatalyze

Prashant built Locatalyze to make rigorous location analysis accessible to every Australian operator, in every market.

Tools first — then a full report for your address

Free rent, viability, and break-even checks. Upgrade when you are ready for competitors, map, and numbers for a specific site.

No signup required for tools